Introduction

Buying a home in Ohio might be one of the biggest financial decisions you’ll ever make. Whether you’re eyeing a charming Victorian in Cincinnati, a modern condo in Columbus, or a lakefront property in Cleveland, understanding current mortgage rates Ohio lenders offer can save you thousands of dollars over the life of your loan.

Right now, mortgage rates are constantly shifting based on economic factors, Federal Reserve decisions, and market conditions. What you saw last month might be completely different today. That’s why staying informed about current mortgage rates Ohio banks and credit unions provide is absolutely crucial for making smart financial decisions.

In this comprehensive guide, you’ll discover everything about current mortgage rates Ohio homebuyers face today. We’ll explore what rates look like right now, factors that influence them, how Ohio compares to national averages, and strategies to secure the best possible rate. You’ll also learn about different loan types, how to improve your chances of approval, and which lenders offer the most competitive rates in the Buckeye State.

What Are Current Mortgage Rates in Ohio?

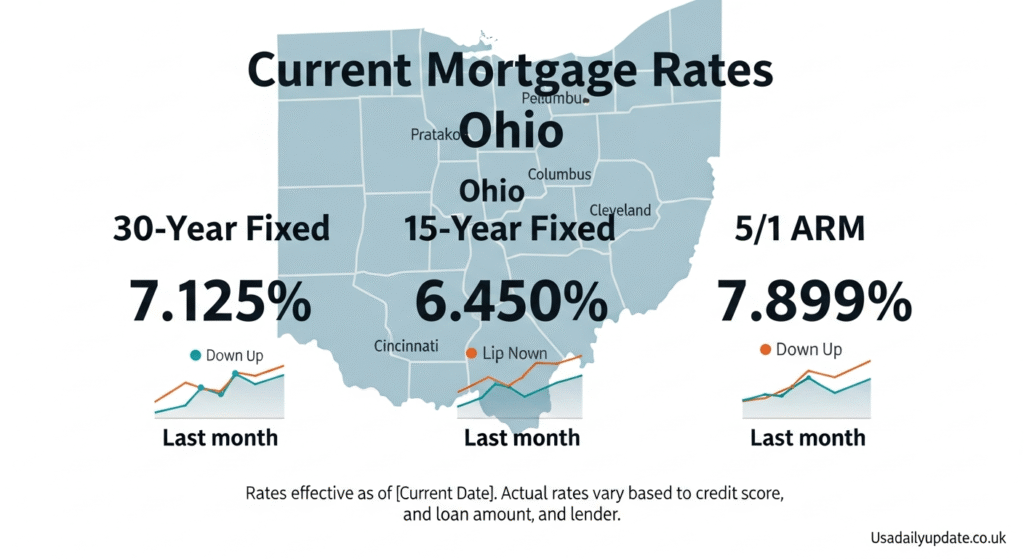

Current mortgage rates Ohio residents can expect vary depending on several factors. As of early 2025, rates have stabilized somewhat after the volatility of previous years. Understanding where rates stand today helps you make informed decisions about timing your home purchase.

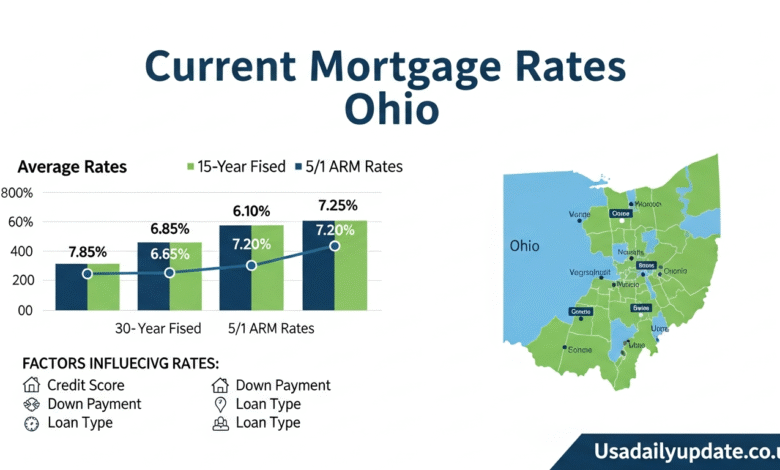

For a 30-year fixed-rate mortgage, Ohio rates typically hover in a competitive range. These rates represent what borrowers with excellent credit can expect to pay. Your actual rate may differ based on your financial profile, down payment, and chosen lender.

The 15-year fixed-rate mortgages generally come with lower rates than their 30-year counterparts. These shorter-term loans appeal to buyers who want to build equity faster and pay less interest overall. The trade-off is higher monthly payments.

Adjustable-rate mortgages (ARMs) often start with lower initial rates than fixed mortgages. These can be attractive if you plan to move or refinance within a few years. However, they carry the risk of rate increases after the initial fixed period ends.

Keep in mind that advertised rates represent the best-case scenarios. Lenders quote these for borrowers with credit scores above 740, down payments of 20% or more, and strong debt-to-income ratios. Most borrowers won’t qualify for the absolute lowest rates but can still find competitive options.

Factors That Influence Your Mortgage Rate in Ohio

Understanding what determines your interest rate empowers you to take action. Several key factors influence the current mortgage rates Ohio lenders will offer you specifically. Some you can control, while others depend on broader economic conditions.

Your Credit Score Matters Most

Your credit score is perhaps the single most important factor in determining your rate. Lenders view higher scores as indicators of responsible borrowing behavior. Someone with a 760 credit score might receive a rate a full percentage point lower than someone with a 640 score.

This difference translates to significant money over time. On a $300,000 mortgage, just one percentage point difference means paying tens of thousands more in interest. Improving your credit score before applying for a mortgage can literally save you the cost of a car.

Check your credit reports from all three bureaus well before applying. Dispute any errors you find. Pay down existing debts and avoid opening new credit accounts in the months before your application.

Down Payment Size

The amount you put down affects your rate substantially. Lenders consider larger down payments less risky since you have more equity in the property immediately. A 20% down payment typically secures better rates than putting down just 3% or 5%.

Additionally, down payments below 20% usually require private mortgage insurance (PMI). This added cost increases your monthly payment even beyond the interest rate. If possible, saving for a larger down payment benefits you in multiple ways.

Some buyers use gifts from family members to boost their down payment. Others tap into first-time homebuyer programs that Ohio offers. These strategies can help you reach that 20% threshold more quickly.

Loan Type and Term Length

Different loan products come with different rates. Conventional loans, FHA loans, VA loans, and USDA loans all have unique rate structures. Conventional loans typically offer the best rates for borrowers with strong credit and substantial down payments.

Government-backed loans like FHA might have slightly higher rates but accept lower credit scores and down payments. VA loans for veterans often feature competitive rates with no down payment required. USDA loans for rural properties also offer attractive terms.

The term length you choose impacts your rate significantly. Shorter terms like 15 years have lower rates but higher monthly payments. Longer terms like 30 years spread payments out, making them more manageable monthly but costing more in total interest.

Debt-to-Income Ratio

Lenders calculate your debt-to-income ratio (DTI) by dividing your monthly debt obligations by your gross monthly income. They want to see that you have sufficient income to handle your mortgage payment alongside existing debts.

Generally, lenders prefer DTI ratios below 43%, though some programs accept higher ratios. A lower DTI demonstrates financial stability and can help you qualify for better rates. Paying down credit cards and other debts before applying improves your DTI.

If your ratio is borderline, consider ways to increase your income or reduce debts before applying. Even small improvements can make a difference in your rate and monthly payment.

Property Type and Location

The property itself influences your rate. Single-family homes typically get better rates than condos or multi-unit properties. Primary residences receive lower rates than investment properties or second homes.

Location within Ohio matters too. Properties in stable, growing neighborhoods may qualify for slightly better terms. Lenders also consider the property’s condition, as homes requiring significant repairs might face higher rates or additional requirements.

How Ohio Mortgage Rates Compare Nationally

You might wonder how current mortgage rates Ohio lenders offer stack up against national averages. Generally, Ohio rates align closely with national trends, though regional economic factors create some variation.

Ohio’s housing market has remained relatively stable compared to boom-and-bust cycles in coastal states. This stability contributes to competitive mortgage rates. Lenders view the Ohio market as lower risk than areas with extreme price volatility.

The state’s diverse economy, featuring healthcare, manufacturing, education, and technology sectors, provides economic resilience. This diversification reassures lenders about employment stability, potentially translating to favorable rates for borrowers.

Cost of living in Ohio is generally lower than national averages. This means your dollar goes further, and lenders recognize that borrowers face lower overall expenses. Home prices in most Ohio markets remain accessible compared to states like California or New York.

Competition among lenders in Ohio is robust. The state hosts numerous national banks, regional banks, credit unions, and online lenders. This competition benefits consumers through competitive rates and diverse product offerings. Shopping around pays off in Ohio’s competitive lending landscape.

Types of Mortgage Loans Available in Ohio

Understanding different loan types helps you find the best fit for your situation. Each program has unique features, qualification requirements, and rate structures. Let’s explore the most common options for securing current mortgage rates Ohio buyers use.

Conventional Loans

Conventional mortgages aren’t backed by government agencies. They follow guidelines set by Fannie Mae and Freddie Mac. These loans work well for borrowers with good credit and stable income.

Conventional loans require minimum credit scores around 620, though better rates come with higher scores. Down payments can be as low as 3% for first-time buyers, though 20% down avoids PMI. These loans offer flexibility in property types and loan amounts.

If you have strong finances, conventional loans typically offer the best current mortgage rates Ohio lenders provide. They also allow you to cancel PMI once you reach 20% equity, unlike FHA loans where mortgage insurance can last the loan’s lifetime.

FHA Loans

Federal Housing Administration loans help borrowers who might not qualify for conventional financing. They accept credit scores as low as 580 with 3.5% down, or 500 with 10% down. This accessibility makes them popular for first-time buyers.

FHA loans require both upfront and annual mortgage insurance premiums. The upfront premium is 1.75% of the loan amount, typically rolled into the loan. Annual premiums continue for the loan’s life if you put down less than 10%.

While FHA rates might be slightly higher than conventional rates, the easier qualification makes homeownership accessible to more Ohioans. If you have limited savings or credit challenges, FHA loans provide a viable path to homeownership.

VA Loans

Veterans, active-duty service members, and eligible surviving spouses can access VA loans. These government-backed mortgages require no down payment and no private mortgage insurance. This makes them incredibly valuable for those who qualify.

VA loans typically offer competitive rates comparable to or better than conventional loans. The VA guarantees a portion of the loan, reducing lender risk. This benefit passes to borrowers through favorable terms.

There is a VA funding fee, but it’s lower than FHA insurance premiums and can be rolled into the loan. Disabled veterans may qualify for fee exemptions. If you’re eligible for VA benefits, this loan type should be your first consideration.

USDA Loans

The U.S. Department of Agriculture backs loans for rural and suburban properties. Ohio has many areas that qualify under USDA definitions of rural, including some suburban communities near cities.

USDA loans require no down payment and offer competitive rates. They’re designed for low-to-moderate income buyers purchasing in eligible areas. Income limits apply based on household size and county.

These loans require both upfront and annual guarantee fees, similar to FHA loans. However, the no-down-payment feature makes homeownership accessible for families who struggle to save large sums. Check USDA’s eligibility map to see if your desired area qualifies.

Best Mortgage Lenders in Ohio

Finding the right lender is as important as securing good rates. Ohio offers numerous excellent lending institutions, each with strengths in different areas. Here are some top options for current mortgage rates Ohio borrowers should consider.

National Banks

Large national banks like Chase, Bank of America, and Wells Fargo operate extensively in Ohio. They offer comprehensive services, advanced technology, and the security of established institutions. Their rates are competitive, especially for existing customers.

These banks provide convenience through extensive branch networks and robust online platforms. You can often manage your entire mortgage process digitally. They also offer relationship discounts if you have checking accounts or other products with them.

The downside is sometimes less personalized service compared to smaller institutions. Your loan officer might handle dozens of clients simultaneously. However, their efficiency and resources often compensate for this through smooth, streamlined processes.

Regional Banks

Ohio-based banks like Huntington Bank, KeyBank, and Fifth Third Bank understand the local market intimately. They have deep roots in Ohio communities and often provide exceptional customer service.

Regional banks might offer more flexibility in underwriting decisions. They understand Ohio’s neighborhoods, economy, and housing markets better than out-of-state institutions. This local expertise can benefit borderline applications.

Rates from regional banks compete closely with national lenders. They sometimes offer special programs for Ohio residents or first-time buyers. Their combination of local knowledge and competitive pricing makes them excellent options.

Credit Unions

Credit unions like Wright-Patt Credit Union, GE Credit Union, and Ohio Educational Credit Union serve members with competitive rates and lower fees. Credit unions are not-for-profit, allowing them to pass savings to members.

Membership requirements vary by institution. Some serve specific employers, regions, or affiliated groups. Once you join, you often receive personalized service and competitive current mortgage rates Ohio credit unions pride themselves on.

Credit unions typically offer more flexible qualification criteria than traditional banks. They might consider factors beyond credit scores, understanding individual circumstances. This human approach benefits borrowers with unique situations.

Online Lenders

Digital mortgage companies like Rocket Mortgage, Better.com, and LoanDepot offer streamlined online experiences. They use technology to reduce overhead costs, potentially passing savings to borrowers through competitive rates.

The application process is typically fast and convenient, manageable entirely from your phone or computer. You receive quick pre-approvals and can track your loan status in real-time. This appeals to tech-savvy buyers who prefer digital interactions.

However, online lenders lack physical branches for in-person consultations. Some borrowers prefer face-to-face guidance, especially first-timers navigating complex processes. Weigh convenience against the value of personal interaction when choosing.

How to Get the Best Mortgage Rate in Ohio

Securing the lowest possible rate requires strategy and preparation. Here are proven steps to improve your chances of obtaining the best current mortgage rates Ohio lenders offer.

Improve Your Credit Score

Start by checking your credit reports from all three bureaus. Dispute any errors immediately, as these can unfairly lower your score. Focus on factors within your control: pay all bills on time, reduce credit card balances, and avoid new credit inquiries.

Aim to get your credit utilization below 30% of your available credit limits. Even better, keep it under 10% if possible. This demonstrates responsible credit management and can boost your score significantly.

Give yourself time for these improvements to reflect in your score. Major positive changes might take several months. Starting early in your homebuying journey maximizes your ability to qualify for the best rates.

Save for a Larger Down Payment

Every extra dollar you save for down payment potentially improves your rate and reduces your overall costs. Set up automatic transfers to a dedicated savings account. Cut unnecessary expenses and redirect that money toward your home fund.

Consider gift funds from family members, which most lenders accept with proper documentation. Avoid large deposits without clear paper trails, as lenders scrutinize unexpected funds during underwriting.

Some Ohio programs help first-time buyers with down payment assistance. Research options through Ohio Housing Finance Agency and local housing authorities. These programs can supplement your savings significantly.

Shop Multiple Lenders

This is perhaps the most important step. Different lenders offer different rates even on the same day for the same borrower profile. Comparing multiple quotes ensures you find the best deal available to you.

Apply to at least three to five lenders within a two-week window. Credit bureaus recognize mortgage shopping and count multiple inquiries in a short period as a single hit to your credit score.

Don’t just compare interest rates. Look at annual percentage rates (APRs), which include fees and other costs. Compare closing costs, lender fees, and loan terms. Sometimes a slightly higher rate with lower fees costs less overall.

Consider Rate Locks

Once you find a favorable rate, consider locking it in. Rate locks guarantee your rate for a specified period, typically 30 to 60 days. This protects you from rate increases while your loan processes.

Some lenders offer float-down options, allowing you to capture lower rates if they drop after locking. This feature provides flexibility but might cost extra. Weigh the cost against potential benefits based on rate trends.

Timing your rate lock requires balancing protection against flexibility. Lock too early, and you might miss rate drops. Lock too late, and increases could cost you. Discuss optimal timing with your loan officer based on your specific situation.

Negotiate and Ask Questions

Don’t accept the first offer without discussion. Ask lenders if they can match or beat competitors’ quotes. Many will adjust their initial offers to win your business, especially if you have strong qualifications.

Question every fee on your loan estimate. Some fees are negotiable while others are fixed. Understanding what you’re paying for helps you compare offers accurately and potentially negotiate reductions.

Build relationships with loan officers. Responsive, knowledgeable professionals can guide you toward better deals and smoother processes. Don’t hesitate to ask questions about anything you don’t understand fully.

Understanding Mortgage Rate Trends in Ohio

Staying informed about rate trends helps you time your purchase optimally. While nobody can perfectly predict future rates, understanding factors that influence them provides valuable context.

Economic Indicators

Mortgage rates closely follow the 10-year Treasury yield. When Treasury yields rise, mortgage rates typically follow. Economic strength, inflation concerns, and Federal Reserve policy all influence Treasury yields.

Employment data, GDP growth, and consumer spending reports impact rate movements. Strong economic data can push rates higher as investors anticipate Federal Reserve rate increases. Weak data might lower rates as investors seek safe-haven investments.

Following these indicators doesn’t require becoming an economist. Simply staying aware of major economic reports and Federal Reserve announcements helps you understand rate movements.

Federal Reserve Actions

The Federal Reserve doesn’t directly set mortgage rates, but its policies significantly influence them. When the Fed raises or lowers the federal funds rate, it affects overall borrowing costs throughout the economy.

Recent Fed policy focused on controlling inflation through rate increases. As inflation moderates, the Fed might adjust its stance. These policy shifts ripple through mortgage markets, affecting current mortgage rates Ohio borrowers encounter.

Fed meetings occur regularly throughout the year. Their statements and press conferences provide insights into future policy direction. Watching these helps you anticipate potential rate movements.

Housing Market Conditions

Local housing market strength affects rates indirectly. When housing demand is strong and inventory low, like in many Ohio markets recently, upward pressure on home prices can influence lending conditions.

Ohio’s housing inventory has improved somewhat from extreme lows, creating more balanced market conditions. This balance benefits buyers through more choices and potentially more favorable lending terms.

Seasonal patterns also affect rates, though less dramatically than economic factors. Spring and summer typically see more homebuying activity. Planning purchases during slower seasons might provide slight advantages.

First-Time Homebuyer Programs in Ohio

Ohio offers several programs specifically designed to help first-time buyers overcome common obstacles. These programs can make securing favorable current mortgage rates Ohio buyers need more achievable.

Ohio Housing Finance Agency Programs

OHFA provides down payment assistance and competitive interest rates to eligible buyers. Their programs help with down payments and closing costs, which are often the biggest barriers to homeownership.

Qualification requirements include income limits based on county and household size. You must complete homebuyer education, which actually benefits you by preparing you for homeownership responsibilities.

OHFA works with approved lenders throughout Ohio. Ask potential lenders if they participate in OHFA programs. These programs can be combined with FHA, VA, USDA, and conventional loans.

Local Housing Programs

Many Ohio cities and counties offer additional assistance. Columbus, Cleveland, Cincinnati, and other communities have programs providing grants, forgivable loans, or favorable terms to buyers in specific areas.

These local programs often target neighborhood revitalization or workforce housing. They might offer significant financial help but require you to purchase in designated areas and meet income requirements.

Research programs through your city or county housing department. These resources complement state programs, potentially providing substantial combined assistance.

Tax Credits and Deductions

Ohio first-time buyers might qualify for federal mortgage interest deductions, which reduce taxable income. While tax laws change, these deductions have historically provided significant savings for homeowners.

Some first-time buyers qualify for Mortgage Credit Certificates through OHFA. These convert part of mortgage interest into a dollar-for-dollar tax credit, providing ongoing savings more valuable than deductions.

Consult with tax professionals about homeownership tax benefits applicable to your situation. These savings effectively reduce your homeownership costs, making slightly higher rates more affordable.

Refinancing Mortgage Rates in Ohio

If you already own a home in Ohio, understanding refinancing rates helps you decide whether refinancing makes sense. Many homeowners refinance to lower payments, shorten loan terms, or access equity.

When Refinancing Makes Sense

The traditional rule suggests refinancing when you can reduce your rate by at least 1%. However, even smaller reductions might justify refinancing if you plan to stay in your home long enough to recoup closing costs.

Calculate your break-even point by dividing closing costs by monthly savings. If you’ll stay in your home longer than this break-even period, refinancing likely makes financial sense.

Beyond rate reduction, refinancing can eliminate PMI once you have 20% equity. It can also convert ARMs to fixed-rate mortgages, providing payment stability. Some homeowners refinance to access equity for renovations or debt consolidation.

Cash-Out Refinancing

Cash-out refinancing lets you borrow against your home equity. Ohio homeowners with substantial equity can access funds for various purposes while potentially securing better rates than their original mortgages.

This option works well for major expenses like home improvements, which can increase property value. Rates on cash-out refinances are typically slightly higher than rate-and-term refinances but much lower than credit cards or personal loans.

Consider the long-term implications carefully. You’re converting equity back into debt, which extends the time you’ll carry a mortgage. Ensure the purpose justifies tapping your equity before proceeding.

Common Mistakes to Avoid

Understanding pitfalls helps you navigate the mortgage process more successfully. Here are mistakes that can cost you better current mortgage rates Ohio lenders might otherwise offer.

Not Shopping Around

Many borrowers accept the first offer they receive. This mistake potentially costs thousands over your loan’s life. Lenders know many people don’t shop around and might not offer their best rates initially.

The effort required to compare multiple lenders is minimal compared to potential savings. Use online comparison tools, work with mortgage brokers, or directly contact several lenders yourself.

Making Major Financial Changes

Avoid changing jobs, making large purchases, or opening new credit accounts during the mortgage process. Lenders verify your financial situation multiple times, including just before closing.

Significant changes can derail your approval or affect your rate. That new car can wait a few weeks until after closing. Job changes, even promotions, complicate income verification and might delay or jeopardize your loan.

Skipping Pre-Approval

House hunting without pre-approval wastes time and potentially costs you your dream home. Sellers take pre-approved buyers more seriously. In competitive markets, pre-approval can make the difference in whether your offer is accepted.

Pre-approval also clarifies your budget, preventing you from falling in love with homes you can’t afford. The process identifies potential credit issues early, giving you time to address them.

Ignoring Total Costs

Focusing solely on interest rates while ignoring fees, points, and closing costs creates an incomplete picture. A slightly higher rate with lower fees might cost less overall than a lower rate with expensive closing costs.

Always compare APRs, which include most costs, not just interest rates. Review loan estimates carefully, questioning any fees that seem excessive or unclear.

Conclusion

Understanding current mortgage rates Ohio lenders offer empowers you to make informed homebuying decisions. While rates fluctuate based on economic conditions and personal factors, you control many elements that determine your specific rate. Improving credit, saving for larger down payments, and shopping multiple lenders significantly impact the rate you’ll secure.

Ohio’s competitive lending landscape and stable housing market work in your favor. Whether you’re a first-time buyer exploring FHA or OHFA programs, a veteran accessing VA benefits, or an experienced buyer seeking conventional financing, options exist for every situation.

Remember that the lowest advertised rate isn’t always the best deal when you factor in all costs. Focus on finding the right balance of rate, fees, and lender service quality. Take time to understand different loan products and choose what fits your long-term financial goals.

Ready to start your Ohio homebuying journey? Begin by checking your credit, researching current mortgage rates Ohio lenders are offering, and getting pre-approved with multiple institutions. What factors matter most to you when choosing a mortgage lender? Share your thoughts and experiences to help other Ohio homebuyers make confident decisions!

Frequently Asked Questions

What credit score do I need for the best mortgage rates in Ohio? You’ll typically need a credit score of 740 or higher to qualify for the lowest current mortgage rates Ohio lenders advertise. Scores between 670 and 739 receive good rates, while scores below 670 face higher rates or limited options. Improving your score before applying can save thousands in interest.

How much should I put down on a home in Ohio? While 20% down is ideal for avoiding PMI and securing the best rates, many Ohio buyers put down much less. FHA loans accept 3.5% down, conventional loans allow 3% for first-time buyers, and VA or USDA loans require nothing down. Your situation determines the right amount for you.

Are mortgage rates negotiable in Ohio? Yes, mortgage rates have some flexibility. Lenders might match competitor offers, especially for well-qualified borrowers. You can also buy points to lower your rate or negotiate certain fees. Shopping multiple lenders creates leverage for negotiation and helps you find the best deal.

How often do mortgage rates change in Ohio? Mortgage rates can change daily, sometimes multiple times per day, based on economic data and market conditions. Lenders typically update rates each morning. This volatility makes rate shopping time-sensitive and rate locks valuable once you find favorable terms.

What’s the difference between APR and interest rate? The interest rate is the cost of borrowing expressed as a percentage. APR includes the interest rate plus most fees and costs, giving you a more complete picture of loan cost. Always compare APRs between lenders, as this shows the true cost more accurately than interest rates alone.

Should I choose a 15-year or 30-year mortgage in Ohio? This depends on your financial goals and budget. Fifteen-year mortgages have lower rates and build equity faster but require higher monthly payments. Thirty-year mortgages offer lower payments and more flexibility but cost more in total interest. Consider your income stability, other financial goals, and how long you plan to keep the home.

Can I get a mortgage in Ohio with bad credit? Yes, though your options are more limited and rates higher. FHA loans accept credit scores as low as 580, or even 500 with 10% down. Some credit unions and portfolio lenders work with borrowers below these thresholds. Improving your credit before applying will significantly improve your rates and options.

What documents do I need to apply for a mortgage in Ohio? You’ll need recent pay stubs, W-2 forms from the past two years, tax returns, bank statements, photo ID, and documentation of any additional income. Self-employed borrowers need more extensive documentation. Having everything organized before applying speeds up the process considerably.

How long does it take to close on a home in Ohio? Typical closing timelines run 30 to 45 days from accepted offer to closing. This allows time for appraisal, title work, underwriting, and final loan approval. Cash buyers close faster, while certain loan types or complex financial situations might extend the timeline. Your lender will provide a specific timeline.

Are there special programs for rural homebuyers in Ohio? Yes, USDA loans offer zero-down-payment mortgages for eligible rural and suburban properties in Ohio. Many areas qualify that you might not expect, including some communities near cities. Check USDA’s eligibility map and income limits to see if you qualify for this valuable program.

Also Read Usadailyupdate.co.uk